800-538-3767

800-538-3767

As a physician affiliated with UC Davis, you are likely participating in the Group Long Term Disability plan. I am writing this letter to make you aware of the significant limitations inside our plan which may leave us exposed if we were to suffer a disability.

I was recently introduced to InsuranceMD through a colleague of ours who was adamant I speak with them about Long Term Disability Insurance. The agent I spoke with tried to educate me on the importance of having Own Specialty Disability Insurance, but i was convinced I had adequate disability coverage as an employed physician of UC Davis. He then took the time to actually provide me with a complete review of our Long Term Disability benefit and what I learned shocked me and that is why i’m taking this opportunity to share what I learned with you:

- Own Specialty coverage for 1 year ONLY!This policy will pay us for 1 year if a disability prevents us from working in our medical specialty. After 1 years, we will only continue to receive benefits if “the insurance carrier” determines we are unable to perform the duties of “ANY” reasonable occupation

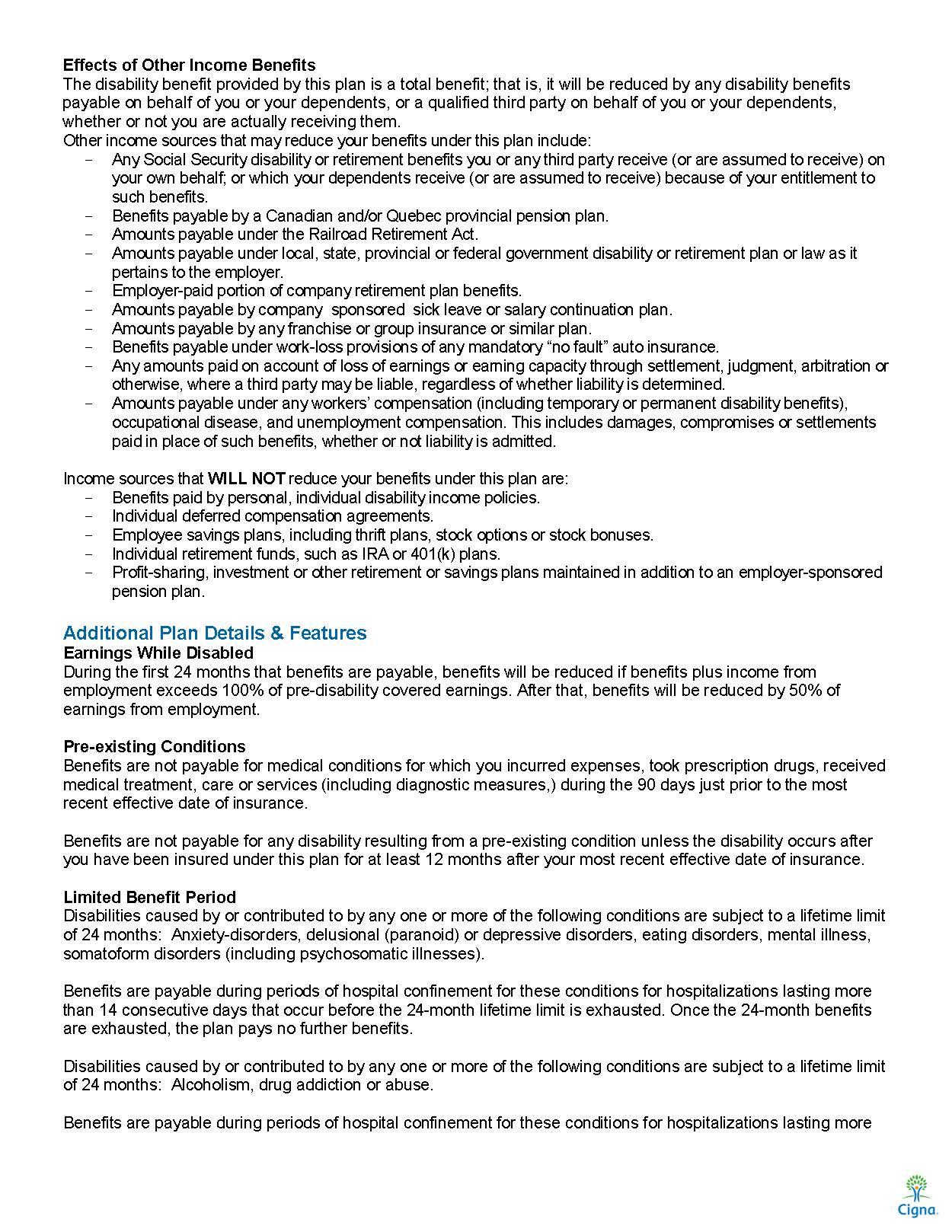

- Our benefits are taxableSince our employer pays the cost of this benefit, if we were to become disabled, we would have to pay income tax on the benefits we received.

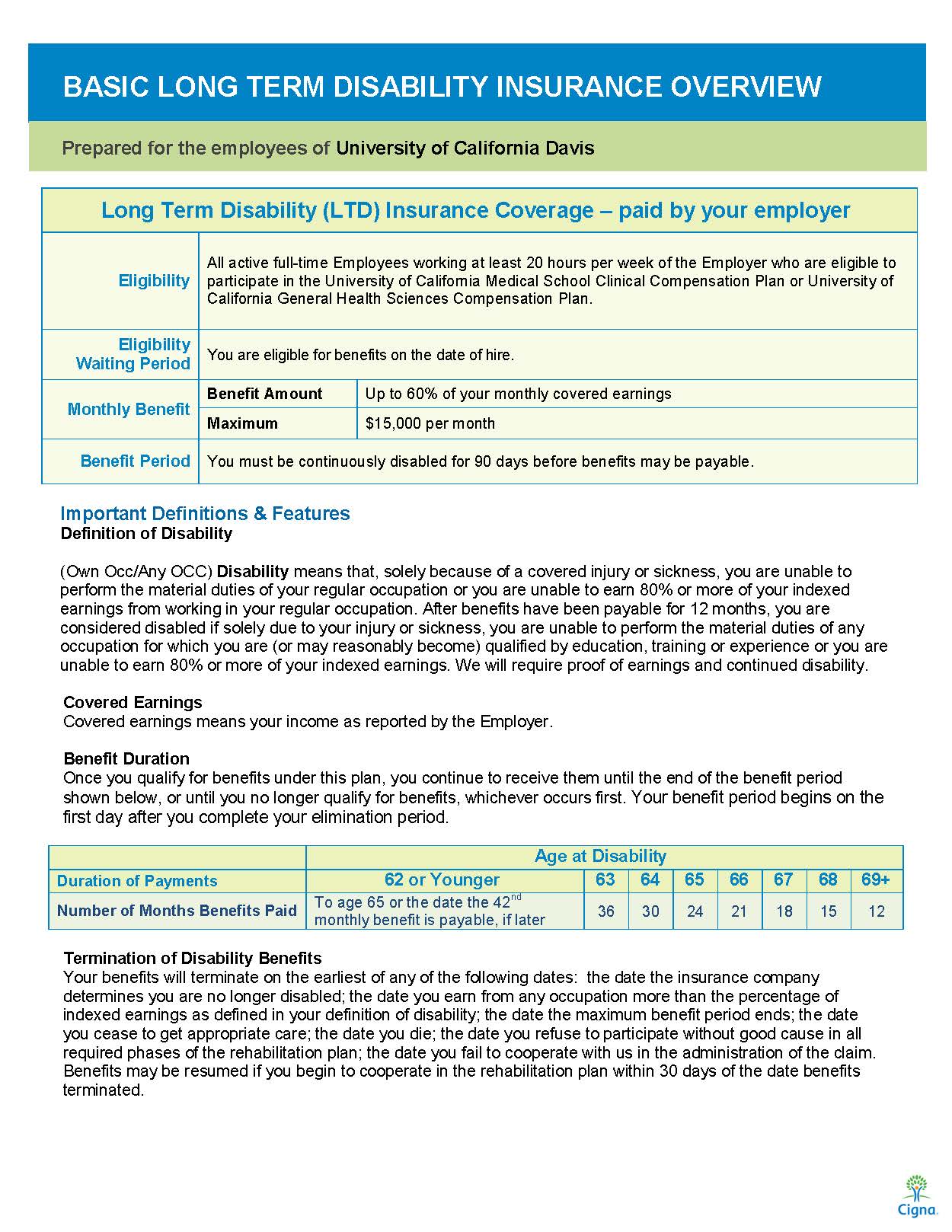

- Coverage is capped at $15,000 per monthUnder our plan, We are eligible for up coverage based off of 60% of our base salary up to a cap not to exceed $15,000 per month of coverage.

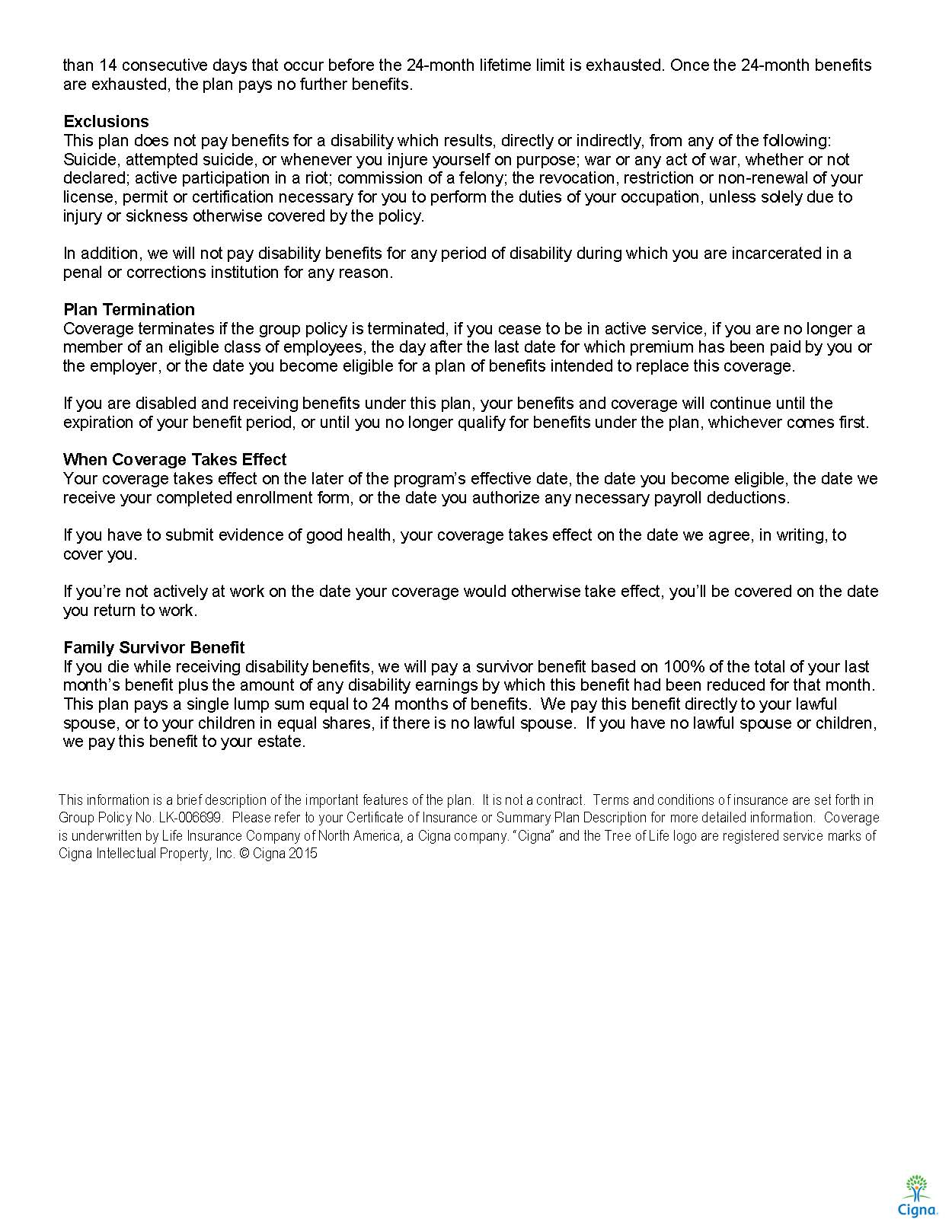

- Our coverage is not guaranteedAccording to our plan. The insurer or UC Davis may cancel our policy at any time based off of a wide variation of reasons as stated in the policy. This leaves us significantly vulnerable to pre-existing conditions if we were to try to obtain coverage elsewhere.

- Only 24 months of coverage for mental healthIf a disability results from a Mental Health Condition, the maximum number of months we may be eligible to receive benefits for is 24 months.

- Our coverage is “NOT” portableOur coverage will terminate if we cease to work at UC Davis. So if we change jobs, and our health has changed, we may not be eligible for coverage in our new job based on pre-existing conditions.

Our UC Davis Disability is Not Own Specialty Coverage

As you can see from above, our UC Davis disability coverage is not adequate for me. I’ve been taught that as a physician, I need Own Specialty Disability Insurance. Our policy gives the insurance carrier the power to determine if we are eligible to work in another occupation within 12 months of becoming disabled in our specialty. As physicians, our policy should also protect our full income, not just the income we earn through our base salary.

Because of these limitations I opted to purchase a supplemental individual Own Specialty policy.

Below is a copy of our UC Davis plan details.

{kind=link}

{kind=link}

As physicians we need “True” Own Specialty Protection.

We should have coverage that provides us with “Tax-Free” income should “any” sickness or injury prevent us from working in our medical speciality. That benefit should allow us to earn income in another occupation without reducing our benefits.

Our disability plan should provide us income protection for both our base and bonus income. Since our health can change as we get older, it’s imperative that our coverage is guaranteed. This means if we leave our employer, our coverage comes with us until we decide we no longer need the protection. Last but certainly not least, our disability provider should never have the power to determine if we are eligible to work in a different occupation and stop paying us our benefits.

Although this coverage comes with a price, the cost of not having it far exceeds what we will pay.

Please take a moment to fill out the form below to speak with the agent who has helped me and others affiliated with UC Davis to obtain “True” Specialty Coverage.

Thank you,

Dr. Emily S

"*" indicates required fields