800-538-3767

800-538-3767

1. When Do I Buy Disability Insurance

The best time to buy disability insurance is when you don’t need disability insurance. In order to qualify for disability insurance, you must first apply for the benefit, so the earlier the better. We encourage that you start with a plan early during your residency when you are at your healthiest. Securing a plan during residency and adding a future purchase option protects your future insurability as your income increases regardless of your health. Even when our nation is not knee-deep in the middle of a pandemic the need for physicians to have True Own Specialty Disability Insurance is more important than ever.

2. What’s the Most Important Feature of a Disability Policy?

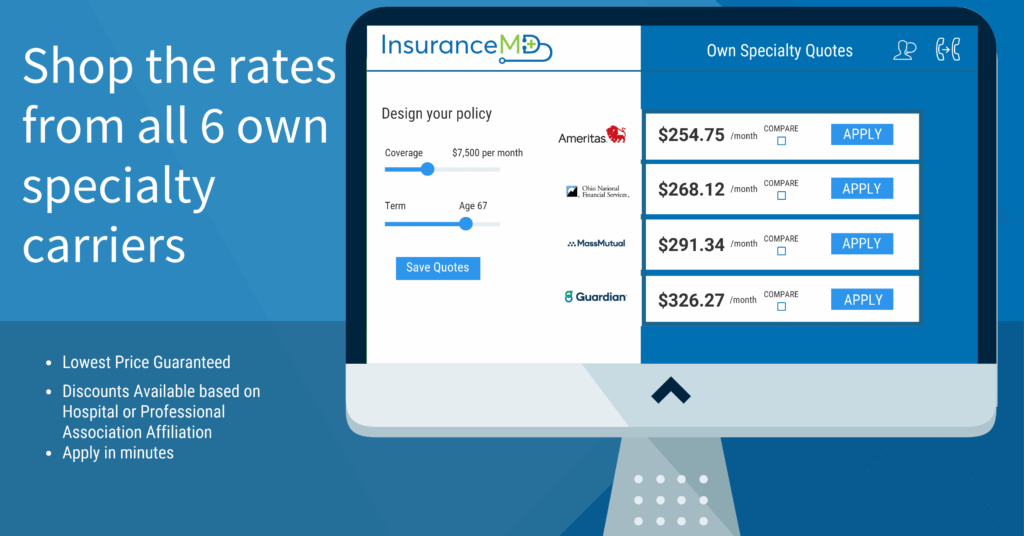

The most important feature of your disability insurance policy is the definition of Total Disability. Total Disability defines when the insurance carrier considers you to be totally disabled and eligible for your full monthly disability benefit. Physicians are advised to obtain a policy with a definition of Total Disability that does not contain language that prohibits you from working in another occupation. Physicians refer to this plan as an Own Specialty Disability policy because the definition of Total Disability will consider you totally disabled even if you elect to work in another occupation. Currently, only six carriers offer such a policy to physicians: Ameritas – Guardian – MassMutual – Ohio National – Principal – The Standard.

3. How Much Disability Insurance Should I Buy?

If you pay for your own private disability policy, your benefits will be paid to you Tax-Free. During your residency, the maximum benefit you are eligible for is $5,000 per month. If you add a Future Purchase Rider you will be permitted to increase your benefit as your income increases regardless of your health. As your income increases so should your disability benefit and the amount you qualify for is based on your income at the time you apply for a new policy or an increase in coverage. The more income you earn, the more disability you should have. As a physician, the maximum combined individual own specialty benefit you can own is $30,000 per month.

4. What Will Disability Insurance Cost Me?

True Own Specialty Disability Insurance is not like the other insurance policies you may be used to paying for. This is a policy that protects your most valuable asset, your income. And according to statistics between 1 in 4 healthy 20-year-olds will suffer a long term disability prior to their retirement age. This explains why it costs so much because it actually gets used. Rates vary based on various different factors: The state you live in, whether you are a male or female, the benefit amount you are eligible for and the riders you add to your policy, and your medical specialty.

The average resident will pay between $180 and $220 per month for a $5,000 per month Own Specialty Disability plan. It’s not uncommon as you increase your monthly benefit as your income rises that you are paying between $600 – $800 per month for your policy. This may come as a shock but it’s a necessary benefit. Until the day comes where you’ve reached financial independence and 100% of your income is considered disposable income you need disability insurance.

5. Are There Any Exclusions?

Prior to qualifying for a disability insurance policy, you must submit to medical underwriting. The insurance carrier will review your medical history to determine if any of your pre‑existing medical conditions will be excluded.

In some cases exclusions are temporary and the carrier may be willing to reconsider an exclusion after some time has passed and your pre-existing medical condition is no longer a risk to the carrier. 1 in 3 disability policies are approved with an exclusion, it’s typical. It’s important to realize that when an exclusion is added to your policy it’s just an exclusion for your pre‑existing condition and that in most cases any new trauma, burn, laceration, or neoplasm that is not caused by your pre‑existing condition will still be considered a covered claim.

If after review of your application they issue you a policy without any exclusions, then you can rest assured that ANY sickness or injury that impacts your ability to work in your occupation will be covered.

Limitations for Mental/Nervous disabilities are part of most contracts where the carrier will only pay your benefit for up to 24 months if your disability is a result of things like anxiety, depression, or substance abuse.

6. What Riders Should I Add to My Policy?

Disability Insurance comes with a handful of riders worth considering. These riders add to the overall cost of your policy but a few of them are crucial for ensuring that your policy will meet your needs should the time ever come where you need it most.

Own Specialty/Regular Occupation Rider – Some carriers make you add the Own Specialty/Own Occupation/Regular Occupation feature to your policy as a rider. The most important feature of your disability policy is the definition of Total Disability. This rider should be mandatory when building your policy.

NonCancellable & Guaranteed Renewable – This available feature protects you from premium increases and contract changes. NonCancellable actually means that the insurance carrier guarantees that your premiums will not increase between your current age and the age of 65. Guaranteed Renewable protects you from the carrier making any contractual changes to your policy ensuring that the features you purchase today will remain the same until you cancel your policy. This provision also guarantees that you have the right to renew your policy every year regardless of your health and regardless of your income.

Residual Disability – This rider should be put on every policy. Residual provides protection from a partial disability that you suffer while you are still working in your medical specialty.

Cost Of Living Adjustment (COLA) – This rider protects you from inflation while you are collecting benefits. We recommend this rider be added if you are between the ages of 20 – 55 where inflation could impact your financial wellbeing during an extended disability.

Future Purchase Option – This rider allows you to increase your benefit at a later date as your income increases regardless of your health.

Catastrophic Disability – This rider provides you an extra benefit above your base monthly benefit should you suffer a serious disability that prevents you from performing 2 out of the 6 activities of daily living.

7. What Carriers Should I Consider?

You should Consider carriers that offer a True Own Specialty Definition of Total Disability. Only Six carriers remain that offer this benefit: Ameritas – Guardian – MassMutual – Ohio National – Principal – The Standard.

Despite what you read or what a captive agent may tell you, carriers like Northwestern Mutual or plans sponsored through your employer or professional medical association like the AMA – ACP – ACOG, etc. do not offer a True Own Specialty Definition for Total Disability because their definition restricts your ability to collect your full benefit if you are working or earning another income in another occupation.

8. I Have a Plan Through My Employer, Isn’t That Good?

Employer-sponsored Long Term Disability Insurance is good enough if your health doesn’t allow you to qualify for your own individual benefit. Having some kind of disability benefit is better than not having any at all. But if you are healthy enough to qualify for Individual Own Specialty Disability Insurance you should buy a plan and here’s why:

Employer-sponsored group disability insurance is not considered True Own Specialty coverage.

The benefit you receive is often taxable.

The contract is not guaranteed.

The coverage may not be portable – but if it is, the premiums will normally increase as you age.

9. When Can I Cancel My Disability Policy?

You can cancel your disability policy at any time. It’s recommended that you keep your disability policy until you retire or until you have reached a point of 100% financial independence and your income is no longer needed to sustain your standard of living.

10. Who Do I Buy a Policy From?

You will want to buy your policy from an independent agent. Shopping the rates and discounts from all 6 carriers is the best way to ensure you are getting the most value from the money you are spending.

The majority of agents will quote between 1 and 3 carriers and try to convince you that 1 of those carriers is best for you. However, the best is different for everyone and every carrier offers virtually identical Own Specialty Plans. So long as you are comparing quotes with the same riders and definitions then the carrier that’s offering you the best price wins.

Here at the White Coat Insurance Group, we provide you with side by side quotes from all 6 carriers so you can rest assured that you are getting the best policy at the best price. We also shop to make certain you are receiving all the discounts you may be eligible to receive based on your Hospital Affiliation or Professional Association Affiliations.